When site selectors, CFOs, and corporate decision-makers evaluate new locations, tax climate is often top of mind. North Carolina has legislated a bold, phased elimination of its corporate income tax, a structural policy move that will reshape how companies project costs and profits in the state.

The Current State: Among the Nation’s Best

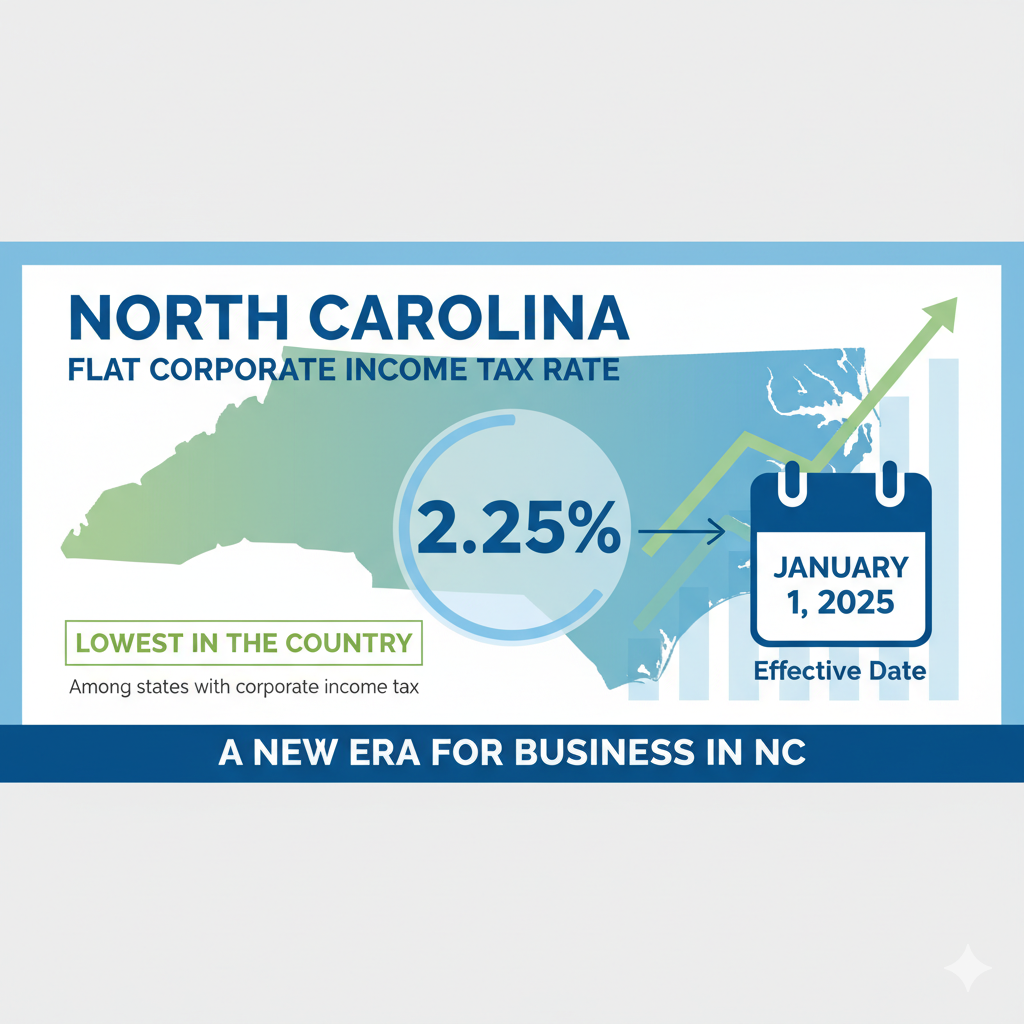

Starting on January 1, 2025, North Carolina’s flat corporate income tax rate was set at 2.25 percent, the lowest in the country among states that still impose a corporate income tax.

This reduction is part of a multiyear phase-out plan. Under current law, the rate is scheduled to decline as follows:

- 2026 → 2.00%

- 2028 → 1.00%

- 2030 onward → 0% (for tax years beginning after 2029)

Because of this trajectory, NC is frequently cited as having the nation’s most competitive corporate income tax in the years before full elimination.

What the Phase-Out Means in Practice

Putting Numbers Behind the Move

Here’s an illustrative example (for C corporations, not pass-through entities—see caveats below):

A business with $10 million in taxable profit in North Carolina would, under a 2.25% rate, owe $225,000 in state corporate tax.

Once the rate is eliminated, that same $10 million would no longer attract a state corporate income tax liability, effectively freeing up that $225,000 for reinvestment, hiring, capital upgrades, etc.

Over a 10-year span, assuming flat profits and full applicability, that’s $2.25 million in potential cumulative tax savings.

Of course, real-world outcomes depend on deductions, apportionment, credits, and business structure. But the baseline math underscores the financial leverage this phase-out creates.

Permanent Plans

Unlike many state incentive programs or abatements that expire or apply only to certain industries, NC plans to eliminate the tax itself permanently for applicable businesses. That makes it a non-expiring structural advantage rather than a temporary subsidy.

When that happens, every dollar of profit subject to NC corporate tax becomes retained earnings (assuming no other state-level tax on corporate profit). In effect, companies get to keep more of their bottom line year after year, without negotiating or renewing incentives.

Beyond Corporate Tax: The Full NC Advantage

Franchise Tax Simplification

Under recent reform, North Carolina restructured its franchise tax regime. C corporations will compute that tax at $1.50 per $1,000 of net worth (with a $200 minimum), eliminating prior property-based bases.

Individual Income Tax Cuts & Structure

The 2023 tax law (S.L. 2023-134) sets the individual income tax at 4.25% for 2025, and schedules it to drop to 3.99% in 2026 (with further reductions possible via revenue triggers).

Retirement & Pension Income

North Carolina excludes Social Security benefits, military pensions, and certain retirement income from state taxation under recent reforms.

Comparative Rates in Other States

Pennsylvania’s corporate tax is 7.99% as of 2025. Many states (especially in the Northeast) maintain rates well above 8%, making NC’s 2.25% a steep discount in comparison.

How This Translates for Brunswick County

For businesses eyeing Brunswick County, the 0% corporate tax path amplifies an already strong value proposition.

Add in:

- Coastal access, port & rail connectivity

- A workforce with lower turnover and strong ties to the locale

- Affordable operational costs and cost-of-living

- Local support via the Brunswick Business & Industry Development team

…and you get a location where more of your profits stay in your business rather than being taxed away.

Framing Disclaimers & Caveats

Pass-through entities (S corps, LLCs, etc.) do not pay corporate income tax—their profits pass through to individual returns. The NC corporate tax and its elimination apply primarily to C corporations. (In fact, many small businesses nationwide are pass-throughs.)

Triggers and revenue thresholds matter. Some rate reductions depend on state revenue meeting benchmarks.

Legislative risk always exists. While the law is in place now, future sessions could alter triggers, delay cuts, or adjust policy based on revenue pressures.

Other taxes still apply: federal taxes, local taxes, property taxes, sales taxes, and compliance costs persist. Zeroing the state corporate tax doesn’t erase those responsibilities.

Taking Action

If your company operates in a high-tax state, the question isn’t whether North Carolina’s tax elimination matters. It’s how quickly you can capitalize on it. The savings are real, immediate, and permanent.

For manufacturers, logistics operators, food processors, and other industries considering expansion or relocation, now is the time to evaluate North Carolina, and specifically Brunswick County, as your next home.

Ready to calculate what 0% corporate tax means for your specific operation? Contact Brunswick Business & Industry Development for customized financial modeling, site tours, and connections to businesses that have already made the move to North Carolina’s coast.